No 6827

Wednesday 3 June 2026

Vol clvi No 32

pp. 505–521

The Council begs leave to report to the University as follows:

1. The Council is required to make an annual Report to the Regent House recommending allocations from the Chest to Schools, institutions and centrally administered funds. Chest allocations and associated Chest expenditure cover the majority of the recurrent pay costs of the University’s academic and professional services posts; however, Chest financial information excludes all research activity, some teaching activity and some other activities.1

2. The University currently forecasts using two different approaches; a bottom-up, Chest-focused planning process linked to available funding sources, and a top-down, overall cash flow model (known as the Ten-Year Model) built from most recent actual results. Enhanced Financial Transparency (EFT), once the new finance system has been brought in, will align bottom-up and top-down planning, meaning institutions can plan on an EFT basis and strategic modelling (at the level of the Finance Committee) can be transparently reconciled to the bottom‑up approach. EFT will be implemented through a phased approach beginning with a two-year initial phase covering the financial years 2027–28 and 2028–29, followed by an embedding phase from 2029–30 to 2032–33 and a steady state model thereafter.2

3. In Easter Term 2027, the University’s finance system will change from CUFS to Oracle Fusion. At the point of the new finance system going live, the accounting basis will change from the historic Chest and related non-Chest to income and expenditure accounting for all activities. Before go-live, prior year financial data will be migrated from the old Chart of Accounts to the new Chart of Accounts, and Schools and institutions will be provided with reconciliation information to allow them to understand how their financial transactions have been translated.

4. During financial year 2026–27, Schools and Non‑School Institutions (NSIs) will update their high-level plans for 2027–28. Alongside this, high-level 2027–28 income and expenditure budgets will be co-created between Finance Division, the Academic Planning and Strategy Office, Schools and Institutions. These will be built using migrated financial data for 2024–25 and 2025–26, as well as inflation assumptions from the Ten-Year Model and material items from School and NSI planning submissions. The resulting budgets will form the basis for the Budget Report for 2027–28, published in the new EFT format covering all income and expenditure.

5. In 2026–27, Schools and NSIs continue to be resourced, in part, via Chest allocations, with the Council continuing to make an annual Report recommending allocations from the Chest to Schools, NSIs and centrally administered funds. This Chest allocations Report is made in the context of both the total Academic University position and the financial outlook of the University Group (including Cambridge University Press & Assessment).

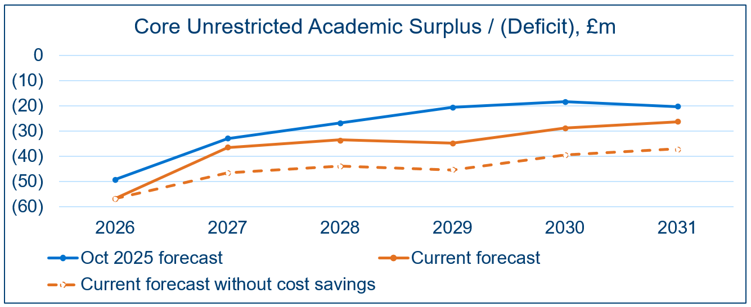

6. The University Group as a whole (including Press & Assessment) generates an annual cash flow surplus from its operations and distributions from the endowment. The operating position for the Academic University remains in overall deficit, however. The overall deficit in 2024–25, as reported to the Finance Committee in October 2025, was £53m. A similar overall deficit is projected for 2025–26. The overall deficit is projected to reduce to ~£35m in 2026–27 and in subsequent years; however, no further, material reductions in the overall Academic University deficit are projected.

7. Tuition fee income is projected to increase significantly due to a higher proportion of international students, and greater numbers of postgraduate taught students. However, these improvements are offset by pay expenditure remaining higher than previously forecast, and higher inflation and energy costs because of the Iran conflict.

8. In 2024 the Council and the General Board endorsed a 5% reduction in overall operating expenditure (Chest and non-Chest), and the PRC and the Finance Committee agreed that a 5% reduction in Chest expenditure would be implemented through a reduction in Chest allocations of 5% for all institutions across 2024–25 and 2025–26 financial years.

9. Schools and institutions have been encouraged to control and reduce expenditure across their entire range of activities. The principal mechanisms to encourage non‑Chest savings in 2025–26 and 2026–27 (i.e. until EFT is brought in) are a 5% overhead to be levied on external trading and Gift Aid3 income, applied to departments with external trading income exceeding £500k p.a.; and a similar levy on the departmental share of research overheads, applied to the departmental share after the usual income allocation policy has been applied to each research grant.4

10. Schools and several non-School institutions have cash reserves which are being used in 2025–26 towards expenditure that would otherwise have been funded from Chest allocations or other, non-Chest funding. An exception is the UAS, which has limited reserves and can only manage within its reduced Chest allocation by reducing expenditure.

11. Until the new finance system, with its new chart of accounts, is brought in, Schools and NSIs are partially resourced via Chest allocations. A practical mechanism to drive achievement of the overall reduction in expenditure endorsed by the Council and the General Board has been a reduction in Chest allocations. Chest allocations to Schools, non-School institutions and centrally administered funds were accordingly reduced by 5% in real terms5 across the 2024–25 and 2025–26 financial years. Those reductions in Chest allocations have in large part been sustained in the proposed Chest budget for 2026–27.

12. Chest allocations are determined by a Chest allocations framework which agrees a baseline and applies an inflation rate aligned to the assumptions for pay and non-pay inflation that drive the Ten-Year Model. The effective rate of inflation on Chest allocations in 2026–27 is 3% for staff costs and 2.5% for non-staff costs. The further inflationary impact of the Iran conflict is difficult to forecast; actual inflation, at least for non-staff costs, may be higher than budgeted, resulting in a further efficiency challenge in these areas.

13. The following paragraphs summarise the current forecast position of the Chest for 2025–26 and 2026–27.

14. Chest income in 2025–26 was budgeted at £647.6m, with the 2025–26 in-year forecast now indicating that income at £654.1m, reflecting a modest increase in the Chest share of income from research grants and contracts, and in CUEF investment income.

15. The principal increase to budgeted Chest income in 2026–27 is an increase in tuition fee income of £38m compared to Chest tuition fees in the 2025–26 Report. This is driven by a higher proportion of international students; greater numbers of Masters-level taught postgraduate students; and increases in unregulated fees.

16. The University’s recurrent funding from Research England and the Office for Students is assumed to be unaltered in 2026–27, pending receipt of grant letters from both organisations in due course.

17. The additional Chest income attributable to the mechanisms for encouraging non-Chest savings, as summarised in paragraph 9 above, is budgeted at approximately £5m.

18. Overall, the combined effect of a budgeted increase in Chest fee income and the expected reductions in Chest expenditure is a projected Chest expenditure deficit in 2026–27 of £10.9m. The Chest expenditure deficit translates to a Chest allocations deficit (Chest income less Chest allocations) of £8m. The impact is summarised in Annex 2.

19. The Resource Management Committee met regularly during Lent Term 2026 to review expenditure plans in Schools and institutions and for centrally administered funds. Planning submissions from each UAS division were reviewed individually, and the RMC was satisfied that each division has credible plans to reduce its expenditure in 2025–26 and to sustain those reductions in 2026–27. The RMC accepted for its part that further, material reductions in professional services expenditure are unlikely without structural and organisational change within the University’s professional services (including those not part of the UAS), which would enable greater rationalisation and economies of scale.

20. The apparently larger increase in the UAS budget than the University budget as a whole is a result of transfers from other budget lines – most significantly the full costs of the in-house model for estates maintenance (for which staff costs are included in the UAS budget, rather than in the centrally administered fund which meets the costs of maintenance projects and contracts); and expenditure to support international student recruitment and admissions, previously funded via the Surplus Improvement Fund.

21. There are a small number of activities whose Chest expenditure is unlikely to be constrained within the expected Chest allocation for 2026–27:

•Cambridge Enterprise required a higher Chest allocation in 2025–26 towards a funding shortfall that has resulted from lower equity realisations. The PRC has agreed that this can continue in 2026–27 pending a review to be led by the incoming Pro‑Vice‑Chancellor for Innovation.

•University Information Services (UIS) has taken several actions to reduce expenditure in 2025–26 and 2026–27 but is constrained to a significant extent by above inflation increases to the costs of software and other licences on which the University relies. UIS’s expenditure plans have been scrutinised by the Information Services Committee and the Resource Management Committee. They have accepted that further, near-term reductions in other IT expenditure, to offset increased software and licencing costs, would be damaging and would undermine the Chief Information Officer’s work in progress to develop and secure agreement for a more financially sustainable basis for delivery of information services across the University. The PRC has made provision – to be held centrally in the first instance – for Chest allocation to cover the projected shortfall.

•The University’s expenditure on insurance is projected to increase in 2026–27, driven principally by a 5% increase in the costs of insurance premiums.

22. In addition, some Schools increased non-regulated tuition fees in 2026–27 beyond the standard rates of increase agreed by the PRC, as a partial alternative to reduced expenditure. The PRC has made provision – once again held centrally in the first instance – for Chest allocation which may be transferred to Schools during 2026–27 to the extent demonstrated by actual student numbers and fee income.

23. The University Group as a whole (including Cambridge University Press & Assessment) continues to generate an annual cash surplus from its operations and distributions from the endowment. The Group’s balance sheet remains strong.

24. The cost base of the Academic University remains high. Cash flow deficits from core academic operations continue to be met from unrestricted reserves, and a failure to deliver a cash surplus from core academic operations leaves the University substantially reliant on Press & Assessment and philanthropy for the capital it needs for investment to remain a world-leading university.

25. Schools and institutions have responded to the requirement to achieve and sustain 5% reductions in overall operating expenditure (Chest and non-Chest). The reduction to Chest allocations to Schools and institutions, and the projected increase in tuition fee income in 2026–27, are the principal drivers for a material reduction in the Chest expenditure deficit and the Chest allocations deficit in 2026–27.

26. Taken in the context of both the University Group and the Academic University’s overall financial position, the Council recommends:

I.That allocations from the Chest for the year 2026–27 be as follows:

(a)to the Council for all purposes other than the University Education Fund: £225.9m.

(b)to the General Board for the University Education Fund: £483.4m.

II.That any supplementary grants from the Office for Students and UK Research & Innovation (through Research England), which may be received for special purposes during 2026–27, be allocated by the Council, wholly or in part, either to the General Board for the University Education Fund or to any other purpose consistent with any specification made by the OfS or UKRI, and that the amounts contained in Recommendation I above be adjusted accordingly.

Annex 1: Chest income and expenditure, including recommended Chest allocations for 2026–27, available at: https://www.admin.cam.ac.uk/reporter/2025-26/weekly/6827/Annex-1.pdf.

Annex 2: Movements from the Chest expenditure deficit for 2025–26 to the Chest allocations deficit for 2026–27, available at: https://www.admin.cam.ac.uk/reporter/2025-26/weekly/6827/Annex-2.pdf.

Annex 3: Business information to support the University budget for 2026–27, available at: https://www.admin.cam.ac.uk/reporter/2025-26/weekly/6827/Annex-3.pdf.

Deborah Prentice, Vice‑Chancellor

Gaenor Bagley

Matthew Copeman

Jo Dekkers

Augustin Denis

John Dix

Heather Hancock

Ella McPherson

Scott Mandelbrote

Ewa Marek

Sally Morgan

Richard Mortier

Mezna Qato

Jason Scott-Warren

Alan Short

Pieter van Houten

Andrew Wathey

Garth Wells

Stephen Wilson

1Chest income comprises unrestricted general income to the University principally from Research England and the Office for Students, student fees and endowment income, and a share of the ‘overhead’ element from research grant income, which is brought into the Chest to offset costs incurred in support of research. Non-Chest income consists principally of research grants, trust funds and other restricted funds, specific donations and trading activity carried out by departments and institutions. It is, for the most part, received and managed directly by relevant local institutions.

2See the Council’s Notice dated 23 April 2026 (Reporter, 6822, 2025–26, p. 438).

3Gift Aid sources of funds which are specifically related to gift aid associated with external trading, for example subsidiaries such as Judge Business School Executive Education Limited (JBSEEL).

4A 5% tax on the departmental share of research overheads will result in a revised share; for example 81% Chest : 19% department for all sponsors other than Industry.

5After allowing for inflation.

The Council begs leave to report to the University as follows:

1. The Council has received a proposed amendment to Grace 1 of 2 April 2026, initiated under Special Ordinance A (ii) 5 by 42 members of the Regent House.1 The Grace recommends that a new provision should be added to Special Ordinance, to enable the General Board to make elections to any vacant Professorship to which the General Board agrees to elect the holder of another Professorship, the election to the vacant Professorship to take effect from the date of resignation from the other Professorship. If the amendment is approved, the Regent House would make the election in such cases following publication of a Report by the General Board.

2. The background information provided with the amendment notes that the amendment is intended to ensure the election is ‘justified’ and that there is no risk of patronage or of lowering academic standards. From this, the Council understands that the primary concern of those who have signed the amendment is with transparency of process.

3. The Council agrees that there should be no lowering of academic standards when making elections in these circumstances. However, it does not agree with the proposers of this amendment that the Regent House is an appropriate body to make decisions on the academic standing of an individual for election to a Professorship. It also does not consider the amendment to be the best way to resolve the concerns about the election process that appear to have prompted it. The Council has therefore included a recommendation in this Report, as an alternative to the amendment from members of the Regent House, in the hope that this allays those concerns but in a way that the Council is willing to support.

4. In the few cases under Part B of Special Ordinance C (vii) where the General Board already makes elections to Professorships, the General Board determines the most appropriate process for making an election, usually on the recommendation of an advisory committee, but not one necessarily constituted as a Board of Electors in accordance with that Special Ordinance nor following a related procedure approved by the Council and the General Board. In the response to remarks at the Discussion of this Report, the General Board confirmed that it would adopt a similar approach when making elections in these circumstances.2 Recommendation II commits the General Board to that process and to publishing the membership of the advisory committee in the Reporter at least 30 days before the Board receives that advisory committee’s recommendation.

5. The Council recommends:

I.That the Regent House approves its decision to withhold authorisation of the initiated amendment, noting the reasons for the Council’s decision as set out in this Report.

II.That if Recommendation I is approved, Special Ordinance C (vii) B. 1(c)(v) (Statutes and Ordinances, 2024, p. 82) be approved to read as follows:

(v)any vacant Professorship to which the General Board agrees to elect the holder of another Professorship on the recommendation of an advisory committee appointed by the Board for that purpose, the membership of which shall be published in the Reporter at least 30 days before the Board considers its recommendation, with the election to the vacant Professorship to take effect from the date of resignation from the other Professorship;

Deborah Prentice, Vice‑Chancellor

Gaenor Bagley

Matthew Copeman

Jo Dekkers

Augustin Denis

John Dix

Heather Hancock

Ella McPherson

Scott Mandelbrote

Ewa Marek

Sally Morgan

Richard Mortier

Mezna Qato

Alan Short

Pieter van Houten

Andrew Wathey

Garth Wells

Stephen Wilson

1For the wording of the Grace and the amendment, including the background information provided with the amendment, see: Reporter, 6821, 2025–26, p. 410.